How Biometric Authentication Protocols Influence Access Tiers in Virtual Card Platform Ecosystems

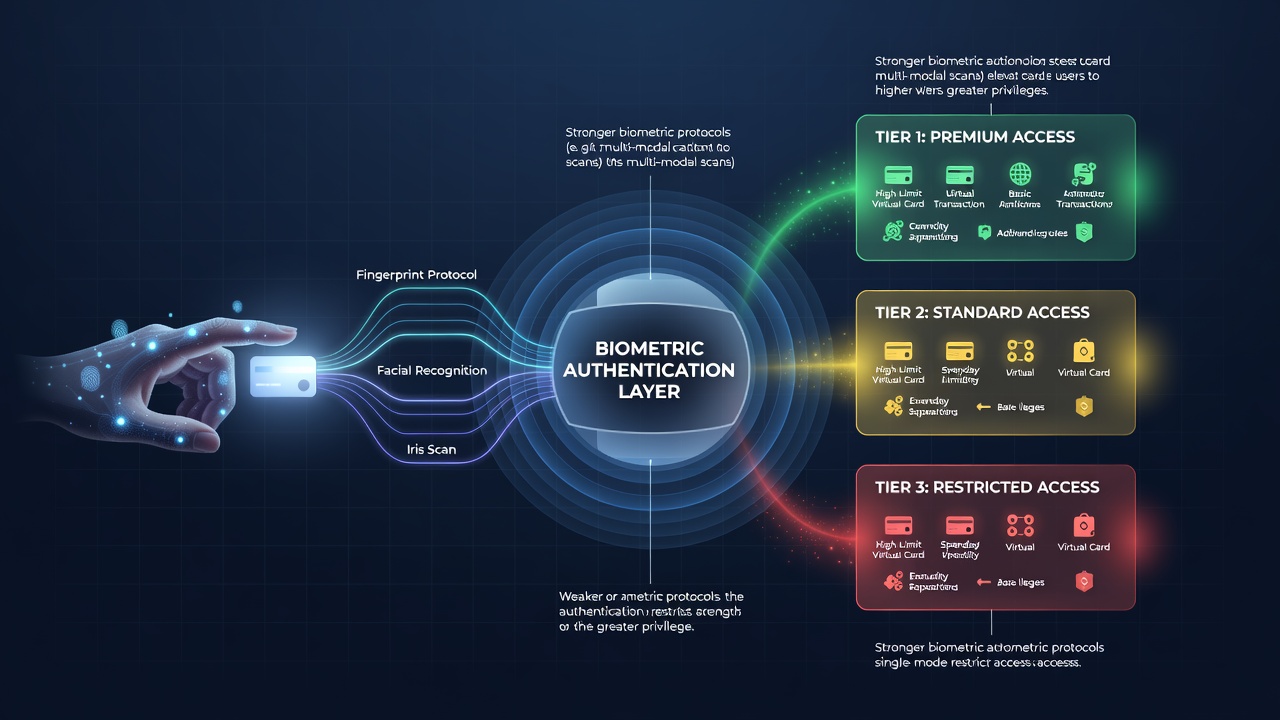

Virtual card platform ecosystems rely on layered authentication methods to manage user access, and biometric protocols have become central to determining which tiers users can reach. These systems assign different permission levels based on verification strength, transaction limits, and feature availability, while biometric data such as fingerprints, facial patterns, and voiceprints serve as the gatekeepers for progression between tiers.

Core Components of Biometric Protocols in Virtual Cards

Biometric authentication protocols operate through standardized frameworks that include template matching, liveness detection, and encrypted storage of biometric data. Platforms integrate these protocols with multi-factor systems so that initial enrollment requires a combination of device-based scans and server-side validation. Researchers at institutions tracking payment security note that protocols aligned with FIDO2 standards reduce reliance on passwords and allow seamless tier upgrades when users demonstrate consistent biometric verification success rates.

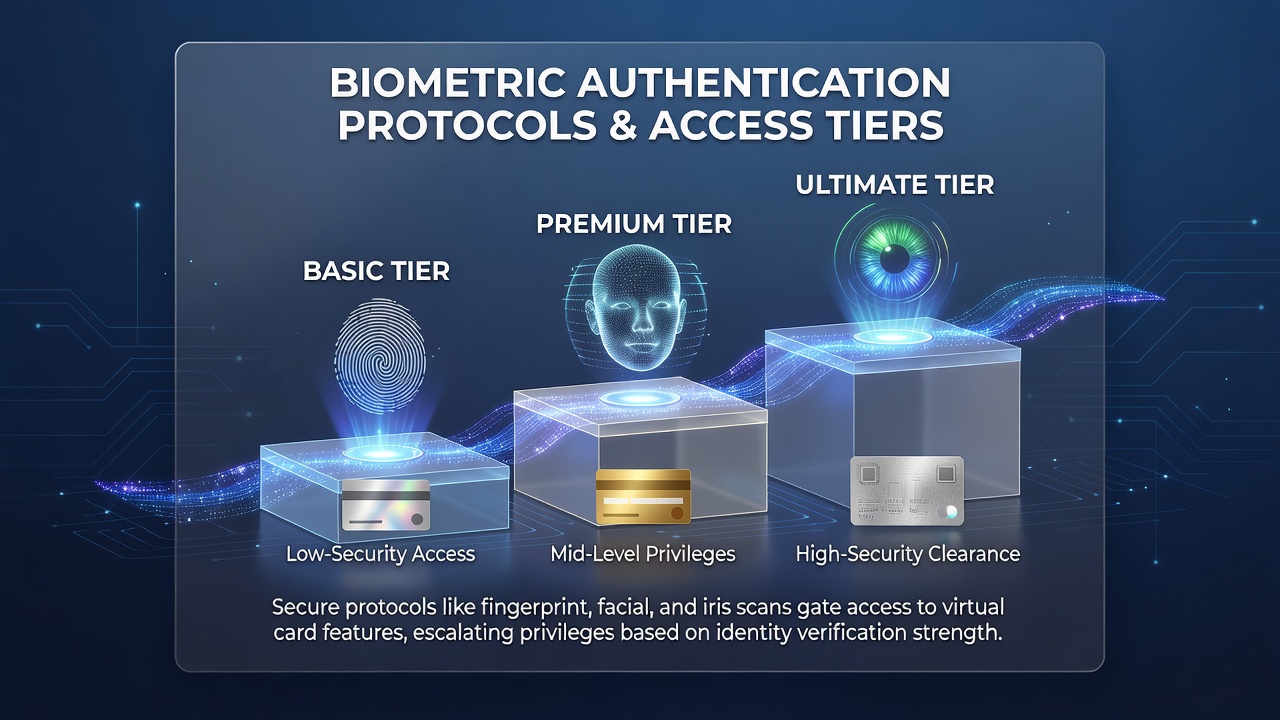

Access tiers typically range from basic entry-level accounts with minimal transaction caps to premium structures that permit high-volume transfers, advanced analytics, and priority support channels. Progression depends on accumulated verification points, and biometric protocols contribute measurable data points such as match confidence scores and session frequency. In June 2026, several platforms updated their tier algorithms to weight recent biometric activity more heavily following reports of evolving fraud patterns across digital payment networks.

How Verification Strength Shapes Tier Eligibility

Platforms evaluate biometric match accuracy against thresholds set by internal risk models. A user completing a high-confidence facial scan during peak hours might receive an automatic elevation to a mid-tier status that unlocks instant virtual card issuance, whereas lower-confidence attempts require additional steps like device attestation. Data from payment industry analyses indicates that such dynamic assessments cut unauthorized access attempts by measurable margins compared to static password systems alone.

Observers note that virtual card ecosystems often link biometric continuity to behavioral signals, including transaction timing and geolocation consistency. When these signals align with successful biometric matches, the system grants access to elevated tiers that include features like real-time spending controls and cross-border transfer options. One documented case involved a regional platform that adjusted its tier matrix after integrating iris recognition, resulting in faster approval cycles for users who maintained consistent biometric profiles over multiple sessions.

Regulatory and Technical Standards Driving Implementation

Technical standards from organizations such as the National Institute of Standards and Technology guide how biometric data must be protected during tier transitions. NIST guidelines emphasize revocable biometric templates and secure key generation, which platforms adopt to maintain compliance while scaling access tiers. European frameworks administered through the European Banking Authority similarly require documented audit trails for biometric decisions that affect user permissions.

Platforms in the Asia-Pacific region reference additional benchmarks from the Australian Cyber Security Centre when designing tier structures. These references ensure that biometric protocols meet regional expectations for data minimization and user consent, allowing smoother cross-border tier recognition for multinational users. Implementation timelines often align with quarterly reviews, and June 2026 saw several operators publish updated compliance reports detailing how biometric confidence thresholds correlate with tier retention rates.

Operational Impacts on User Progression and Platform Security

Once enrolled, users experience tier benefits that scale with biometric reliability. Higher tiers frequently incorporate continuous authentication checks during sensitive operations such as card limit adjustments or merchant onboarding. Evidence from platform telemetry shows reduced account takeover incidents when biometric protocols enforce periodic re-verification at tier boundaries.

Those managing virtual card fleets report that biometric-driven tier systems also support granular delegation, letting primary account holders grant sub-tier access to team members through linked biometric profiles. This approach maintains separation between personal and commercial use cases while preserving the integrity of each tier's risk parameters.

Conclusion

Biometric authentication protocols continue to define the boundaries of access tiers within virtual card platform ecosystems through measurable verification metrics and standardized security practices. As platforms refine their algorithms around confidence scoring and regulatory alignment, the relationship between biometric performance and tier eligibility remains a core operational element across global implementations.